GSTR 9C: Reconciliation Statement & Certification – Filing, Format & Rules

Under the GST regime filing an Annual Return by all GST registered taxpayers, except few, is mandatory. As per the classification of taxpayers and with a view to making the entire system more transparent 3 types of Annual returns have been introduced.

However, here in this blog, we shall know about Reconciliation Statement and Certification- Filing, Format, and Rules related to Annual Return GSTR-9C.

A Short Introduction of GSTR-9C –

As per the GST Act, every person registered under GST, whose annual turnover during a Financial Year exceeds ₹ 2 crores needs to get his/her accounts audited as specified under sub-section (5) of Sec. 35 of the GST Act. A copy of the audited annual accounts and a reconciliation statement, duly certified, should also be furnished in form GSTR-9C.

GSTR-9C is basically a statement of Reconciliation between –

- The Annual Returns in GSTR-9 filed for an FY, and

- The figures as per the audited annual Financial Statements of the taxpayer.

It is something similar to that of a tax audit report dispensed under the Income Tax Act. It consists of gross and taxable turnover as per the Books reconciled with the respective figures as per the consolidation of all the GST returns for a Financial Year. Henceforth, any differences arising from this reconciliation exercise will be reported here along with valid reasons for the same.

The certified statement needs to be issued for every GSTIN. Thus, for a single PAN, there can be several GSTR-9C forms to be filed.

Significant Contents of GSTR-9C –

Form GSTR-9C has of two major parts –

Part-A: Reconciliation Statement

Part-B: Certification

Let us know these both in detail

- Part – A: Reconciliation Statement – It (i.e. Reconciliation Statement) has again been divided into 5 divisions –

Part 1: Basic Details are required to be entered in the following four sections:

1. Financial Year for which the Return is being filed.

2. GSTIN of the taxpayer.

3A. Legal Name of GST registered person.

3B. Trade Name (if any) of the registered business

4. If the taxpayer is liable for any audit under this act?

Note: For FY 2017-18, it will contain details for the period of July 2017 to March 2018.

Part 2: Reconciliation of turnover declared in the Audited Annual Financial Statement with turnover declared in the Annual Return (i.e. GSTR-9):

This includes reporting the gross and taxable turnover declared in the Annual Return with the Audited Financial Statements. One should note that most of the time, the Audited Financial statements are done at PAN level. This might require the breakup of the audited financial statements at GSTIN level for reporting in GSTR-9C. In total, it consists of 18 sections.

Note: Reasons for Un – the Reconciled difference in Annual Gross Turnover:

Valid reasons for non-reconciliation of the annual turnover declared in the audited Annual Financial Statement and turnover as declared in the Annual Return (GSTR 9) should be specified here.

Part 3: Reconciliation of Tax paid:

This section requires GST rate-wise reporting of the tax liability that arose as per the accounts and paid as reported in GSTR-9 respectively with the differences. Furthermore, it requires the taxpayers to state the additional liability because of unreconciled differences noticed upon reconciliation.

Part 4: Reconciliation of ITC availed and utilized:

This part consists of the reconciliation of ITC availed and utilized by taxpayers as reported in GSTR-9 and as reported in the Audited Financial Statement. Moreover, it needs a reporting of Expenses booked as per the Audited Accounts, with a breakup of eligible and ineligible ITC and reconciliation of the eligible ITC with that amount claimed as per GSTR-9. This declaration has to be furnished after considering the reversals of ITC claimed.

Part 5: Recommendation by the Auditor on additional Liability due to non-reconciliation:

Now, the Auditor is liable to report any tax liability identified through the reconciliation process and GST audit, pending for payment by the taxpayer. This can be non-reconciliation of turnover or ITC on account of:

- Amount paid for supplies but not included in the Annual Returns (GSTR-9)

- Incorrect Refund to be paid back

- Other outstanding demands yet to be settled

Finally, the official instructions to the format of GSTR-9C specify that an additional option will be provided to taxpayers to settle taxes as recommended by the auditor at the last stage of the reconciliation of statement.

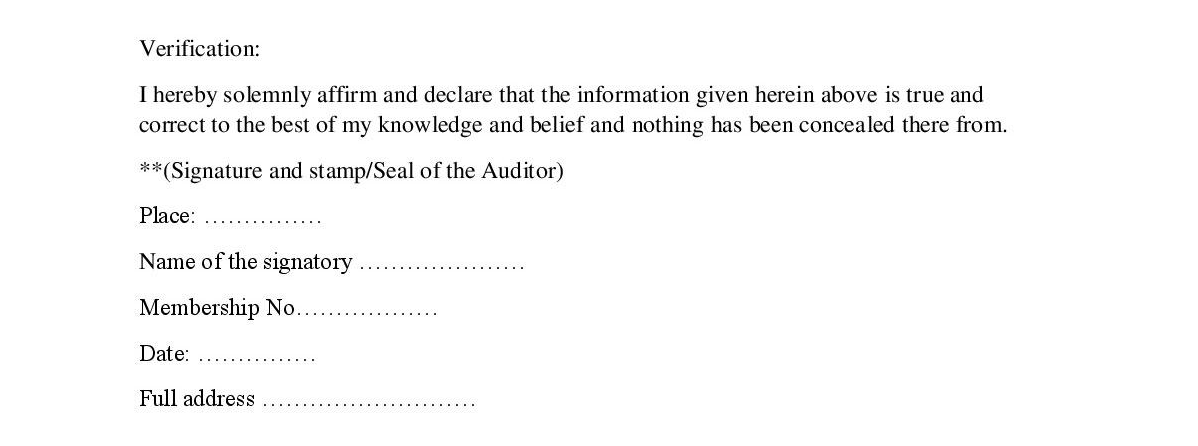

Verification

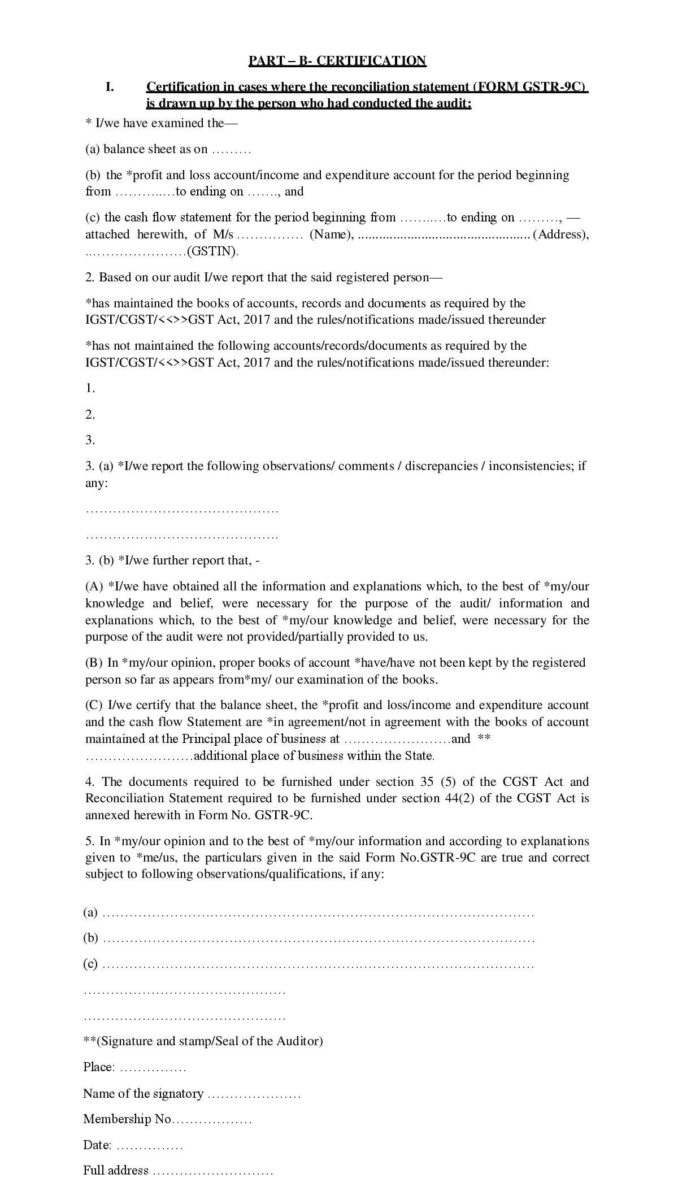

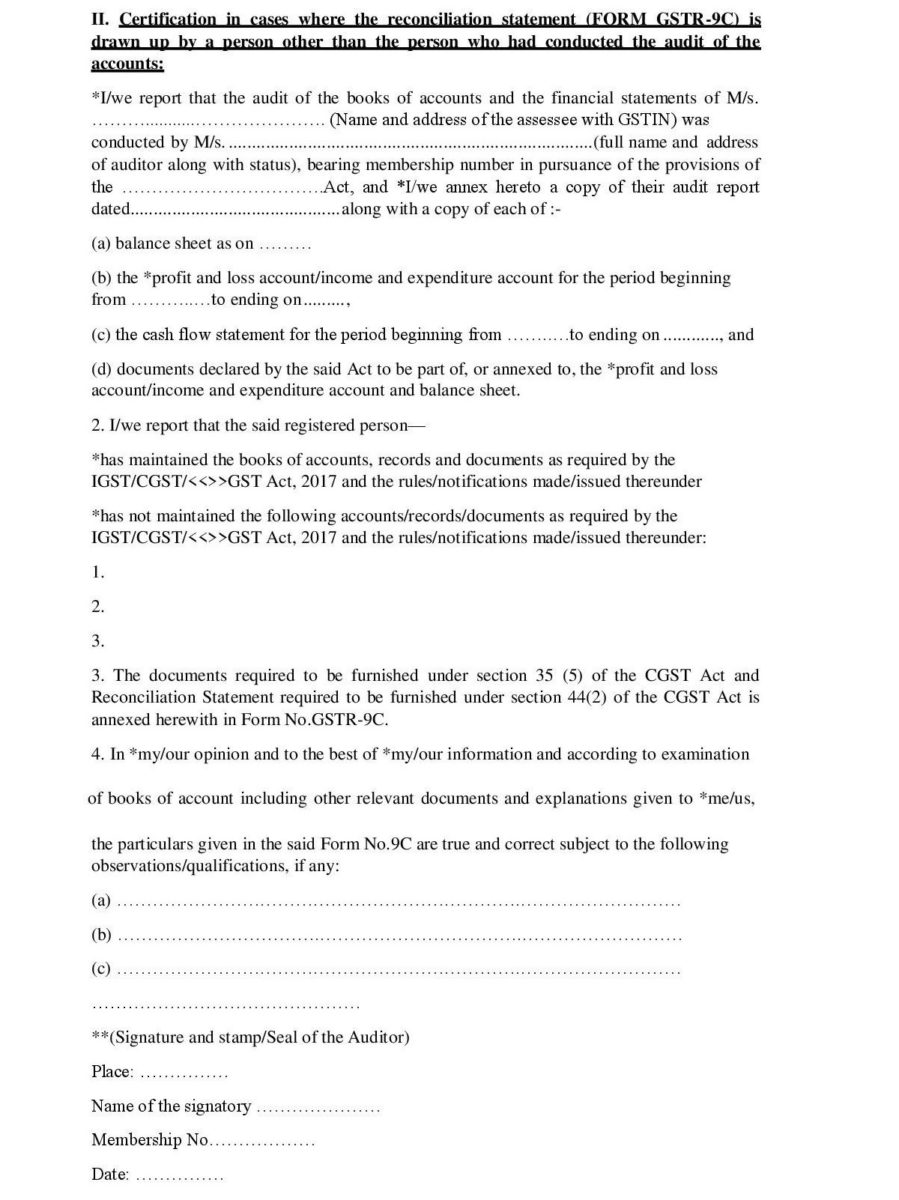

- Part – B: Certification – This has to be certified by a Chartered Accountant or a Cost Accountant –

Form GSTR-9C can be certified by the same CA who conducted the GST audit or it can be also certified by any other CA who did not conduct the GST Audit for that particular GSTIN.

The difference between the both is that in case the CA certifying the GSTR-9C did not conduct the GST audit, he/she should have based the opinion on the Books of Accounts audited by another CA in the reconciliation statement. The format of Part-B for certification report will differ depending on who the certifier is.

Filing of GSTR-9C

- Return to be prepared by Auditor

- Excel tool to be provided for preparation of the return.

- Auditor will generate JSON and handover to the taxpayer after attaching DSC, who will upload the same on the portal.

- Other documents comprising Profit and Loss statement/ Income and expenditure statement etc. also to be uploaded.

- Turnover values will be based on GSTR-9 in few tables.

- A pdf of such values will be made available to the taxpayer. The auditor may have the same from the taxpayer for use in preparing GSTR-9C.

- The file will be processed on the portal and error if any will be indicated. The taxpayer will download the file and handover to Auditor who will make the correction. File to be uploaded again as it was uploaded originally.

- The processed file will be filed by the taxpayer.

- The download option will be available at draft stage and after filing as well in pdf.

- Navigation option to make payment will be available which can be made through GST DRC-03.

Below are some of the most important Rules pertaining to Annual Return GSTR-9C:

- Every GST registered person whose annual turnover during a Financial Year exceeds ₹ 2 crore needs to file GSTR-9C.

- Following persons are not required to file GSTR-9C –

- Casual Taxable Persons.

- Input Service Distributors.

- Non-Resident Taxable persons.

- Persons paying TDS U/s 51 under the GST Act.

- Taxpayers are required to file all the GST returns for all the months of FY 2017-18 in GSTR-1, GSTR-3B, and GSTR – 9.

- GSTR-9C can only be submitted when GSTR-9 has already been filed.

Conclusion

Under the ambit of GST administration, filing of GSTR-9C for the GST registered taxpayers is very important. Getting your accounts certified by a CA is necessary before filing it. While defaulters shall be liable to pay penalty and further complications by the GST department. An unnecessary Demand notice shall be issued instantly. So, to run your business smoothly, it is very important to comply with the GST rules appropriately.

Arpita@HostBooks

Try HostBooks

SuperApp Today

Create a free account to get access and start

creating something amazing right now!